FRODOR

One of Ed Yardeni's great contributions to financial discussions has been his analysis and use of Foreign Official Dollar Reserves (FRODOR). This is defined as US marketable securities held in custody for foreign official and international accounts at the Fed. We've always been impressed with FRODOR's forecasting ability. Visit here to view the correlation between FRODOR and various indexes.

A couple of comments: FRODOR momentum has been declining since 2004. After reaching a cyclical peak of near 35% it has backed off to under 15%. In the past, this decline in momentum has generally coincided with a decline in the US Federal Deficit and an easing in the rate of growth in the US Merchandise Trade Deficit. It has frequently preceded declines in the CRB Raw Industrials Spot Price Index, the CRB Metals Spot Price Index and crude oil demand. With regard to equities, a drop in the FRODOR rate of change typically precedes a drop in S&P 500 forward earnings momentum. Finally, FRODOR seems to have a fairly reliable inverse correlation to the Trade weighted dollar.

Our take: after backing off in 2004 and 2005 from a decade long high, the annual rate of change for FRODOR has churned sideways for a year at a still relatively high level. We think there is a high probability of the decline reasserting itself until it reaches flat year-over-year growth. If so, this would suggest a strong dollar, weak earnings, falling commodity prices and crude oil demand, and falling trade and budget deficits. For more commentary from Yardeni, see this older analysis.

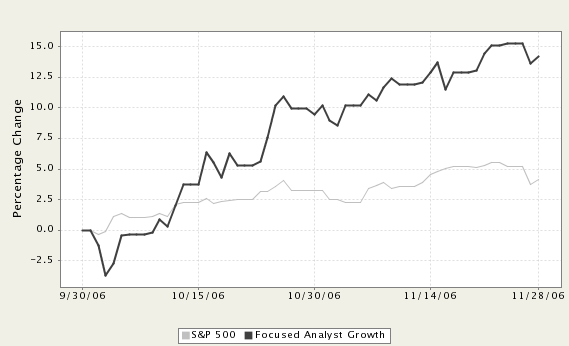

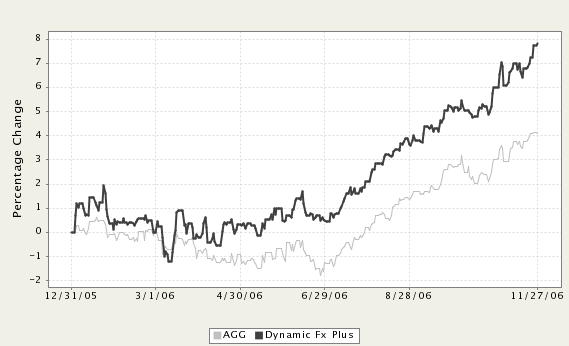

Strategy Update: Equity Opportunity Strategy is a value-based portfolio that is currently up 19.7% YTD through 11/29. The best performers in the Strategy since purchase have been ECA, PRAA, THE, TRX and USG. We continue to think a value strategy makes sense in this environment of private equity capital looking for deals. As always, past performance is not indicative of future results.

A couple of comments: FRODOR momentum has been declining since 2004. After reaching a cyclical peak of near 35% it has backed off to under 15%. In the past, this decline in momentum has generally coincided with a decline in the US Federal Deficit and an easing in the rate of growth in the US Merchandise Trade Deficit. It has frequently preceded declines in the CRB Raw Industrials Spot Price Index, the CRB Metals Spot Price Index and crude oil demand. With regard to equities, a drop in the FRODOR rate of change typically precedes a drop in S&P 500 forward earnings momentum. Finally, FRODOR seems to have a fairly reliable inverse correlation to the Trade weighted dollar.

Our take: after backing off in 2004 and 2005 from a decade long high, the annual rate of change for FRODOR has churned sideways for a year at a still relatively high level. We think there is a high probability of the decline reasserting itself until it reaches flat year-over-year growth. If so, this would suggest a strong dollar, weak earnings, falling commodity prices and crude oil demand, and falling trade and budget deficits. For more commentary from Yardeni, see this older analysis.

Strategy Update: Equity Opportunity Strategy is a value-based portfolio that is currently up 19.7% YTD through 11/29. The best performers in the Strategy since purchase have been ECA, PRAA, THE, TRX and USG. We continue to think a value strategy makes sense in this environment of private equity capital looking for deals. As always, past performance is not indicative of future results.

posted by WRA Strategy Group at 10:21 AM

0 comments

![]()

![]()

{kind=link}

{kind=link}

{kind=link}