Subprime-Loans Getting Ugly

The August 30 edition of the WSJ discusses "the first glimmerings of problems among customers with poor credit." H&R Block has "set aside about $60 million because borrowers were falling behind on their payments. Customers of Countrywide Financial are paying loans off more slowly, as are those at subprime companies Impac Mortgage and Accredited Home Lenders." Mortgage origination volume is also significantly off earlier levels: "First Horizon National said yesterday that mortgage volume was falling so rapidly that it would miss earnings estimates the current quarter."

Another development is that "with the mortgage market slowing and the secondary market for mortgage-related securities faring modestly worse than in the past, investment banks are scrutinizing the loans that come in more carefully." Another problem on the horizon is the rising unpaid balances on Option ARM loans. Investors may need to start worrying about bank's balance sheets and "the industry's lending standards as a whole."

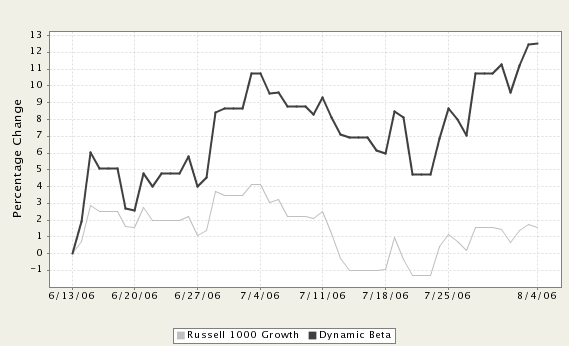

Here's a chart from an article by Robert J. Shiller, an economist at Yale. After the last two peaks in the housing market, prices subsequently went sideways or down for 50 years, adjusted for inflation. This story isn't over - stay tuned. Strategy Update: We've stuck with our long maturity treasury exposure. The treasury market has repeatedly been the investment of choice in times of stress. We see nothing on the short-term horizon to indicate a bottom in the economy or an end to increasing credit worries. Since the interest rate peak in early May our Dynamic Duration Select Strategy is up 7.6% versus the Lehman Aggregate index of 3.1%.

Strategy Update: We've stuck with our long maturity treasury exposure. The treasury market has repeatedly been the investment of choice in times of stress. We see nothing on the short-term horizon to indicate a bottom in the economy or an end to increasing credit worries. Since the interest rate peak in early May our Dynamic Duration Select Strategy is up 7.6% versus the Lehman Aggregate index of 3.1%.

Another development is that "with the mortgage market slowing and the secondary market for mortgage-related securities faring modestly worse than in the past, investment banks are scrutinizing the loans that come in more carefully." Another problem on the horizon is the rising unpaid balances on Option ARM loans. Investors may need to start worrying about bank's balance sheets and "the industry's lending standards as a whole."

Here's a chart from an article by Robert J. Shiller, an economist at Yale. After the last two peaks in the housing market, prices subsequently went sideways or down for 50 years, adjusted for inflation. This story isn't over - stay tuned.

Strategy Update: We've stuck with our long maturity treasury exposure. The treasury market has repeatedly been the investment of choice in times of stress. We see nothing on the short-term horizon to indicate a bottom in the economy or an end to increasing credit worries. Since the interest rate peak in early May our Dynamic Duration Select Strategy is up 7.6% versus the Lehman Aggregate index of 3.1%.

posted by WRA Strategy Group at 7:59 AM

0 comments

![]()

![]()